Dec 28 2006

Buy 130 Intel (Nasdaq: INTC) $20.40

Buy 125 Western Union (NYSE: WU) $22.30

Dec 19 2006

Sell 150 Harrah's Entertainment (NYSE: HET) $81.98

Sell 110 Posco (NYSE: PKX) $83.00

Sell 60 Comcast (Nsadaq: CMCSA) $42.89

Buy 300 Leucadia National (NYSE: LUK) $28.00

Buy 200 Expeditors International of Washington (Nasdaq: EXPD) $41.70

Monday, December 04, 2006

November Update

For the month of November, the portfolio was up 3.8% vs. S&P 500’s 1.9% increase.

A few more earnings trickled. Notably, Tyco (NYSE: TYC) came in with nice results and the breakup is on track for Q1 2007. Heinz's results were quite good and it appears Mr. Peltz's efforts are paying dividend. The company raised its guidance for fiscal 2007.

A few more earnings trickled. Notably, Tyco (NYSE: TYC) came in with nice results and the breakup is on track for Q1 2007. Heinz's results were quite good and it appears Mr. Peltz's efforts are paying dividend. The company raised its guidance for fiscal 2007.The steel sector got a nice boost due takeover speculation and M&A activity. – for now, one announced deal involved

Meanwhile, Comcast (Nasdaq: CMCSA) was busy signing a blockbuster distrobution deal with Disney, buying Disney's stake in the E! Network and last but not least, the company announced plans to raise cable rates. The kind of business we love.

The last day of the month also saw the upgrade of homebuilders by a Banc of America analyst who was gracious enough to slap a “neutral” rating on the sector, whatever that means. Shares of Pulte (NYSE: PHM) and Centex (NYSE: CTX) both got nice boosts as a result.

Finally, we were sad to see Google (Nasdaq: GOOG) leave our portfolio for now. But the price appreciation was much faster than we had anticipated last November when the shares traded at around $400 - they recently hit a high of $513. This opened up room for a new addition in USG Corporation (NYSE: USG) which we recently discussed in more detail on Margin of Safety. USG was itself subject of takeover rumors the same day as Banc of America upgrade of homebuilders.

Happy Holidays. See you in 2007.

Thursday, November 09, 2006

October Update

October ended up being a busy month. The first of week of November was no slouch either. We have a lot to report. Most importantly, we have reached our $200,000 invested capital target. So from here, any cash requirements will be raised through portfolio turnover. For the month of October, the portfolio was up 6.5% vs. S&P 500’s 3.3% increase.

On top of the list has to be Berkshire Hathaway which announced great results and broke through $100,000 for the first time. Mr. Buffett’s bet on a tame hurricane season paid off handsomely. He can stop watching the weather channel now.

Meanwhile, Wendy’s and Tim Horton’s parted ways and we were the beneficiary of our Tim Horton’s shares which have performed well post spin-off and hit an all-time high today. Cisco’s results were a blowout and the stock reflected that today. Morningstar has also rebounded nicely and the earnings report was quite solid. Electronic Arts, Comcast and Google have rallied nicely after beating the Street’s earnings estimates. CBS continued to generate a ton of cash and has announced a sizeable share buyback. Music to our ears.

On the downside,

Other changes during the month were the addition of Harrah’s Entertainment (NYSE: HET) to the portfolio. As I mentioned in a recent post on Margin of Safety, you can think of this as a nice placeholder for some of your cash. There has been no recent news since the initial flurry of activity after the first and only private equity offer of $81 for the company. For now we sit tight on this position. We may trim the position to raise cash if opportunities arise that are too good to pass on. We also took a position in

Wednesday, October 04, 2006

October Trades

Saturday, September 30, 2006

Model Portfolio Launch

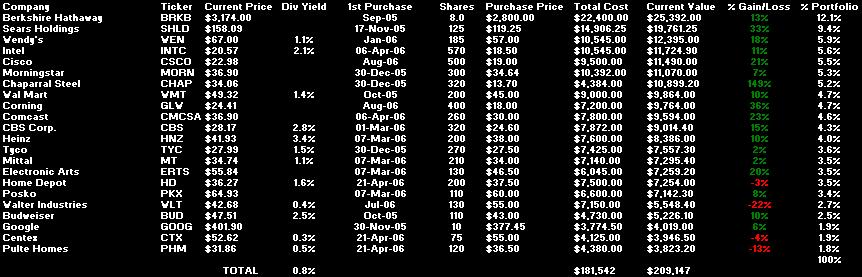

Here it is. The inaugural Margin of Safety Model Portfolio which achieved a 1-year total return of 15.2% vs. S&P 500's 8.5% through the end of September. The portfolio is an eclectic mix of businesses which I am happy to continue holding for now.

Here is a quick update on the holdings.

Berkshire Hathaway (NYSE: BRKA)

Most noteworthy recent news was Mr. Buffett's decision to give his wealth away to various charitable foundations. The main portion went to the Bill and Melinda Gates foundation. He recently visited Israel to meet the founder of Iscar for the first time. Earlier this year he bought 80% of Iscar for $4 billion. While there, he also teased investors by pointing out that Berkshire would likely acquire another 1 to 3 utilities over the next decade. Of interest was a comment about private-equity firms providing Berkshire with some competition for potential investments. No worries. Berkshire has the luxury to wait things out and be approached by the kinds of businesses it covets. Oh, one more thing, Mr. Buffett got married at the end of August to his 29 year companion Astrid Menks.

Sears Holdings (NASDAQ: SHLD)

Eddie Lampert is on the hunt. In the most recent quarterly earnings report, Mr. Lampert couldn't have been any more specific:

"Our strong financial position and cash flow generation provide us with the flexibility to capitalize on a wide range of market opportunities as they arise. In addition to investing in our business and acquiring our shares, we are prepared to invest substantial amounts of capital if we identify other attractive investment opportunities which have the potential for returns we believe appropriately compensate the Company for the associated risks." said Edward S. Lampert, Chairman of Holdings.

Stay tuned.

Wendy's (NYSE: WEN)

The spin-off is complete. On Friday Tim Hortons (NYSE: THI) was officially orphaned and will begin trading as a stand-alone beginning Monday. One more surprise, Timmy's will e added to the S&P/TSX index. This was somewhat unexpected and caught many shorts by surprise. Our bet to invest in the Wendy's shares before the eventual spin-off has paid off handsomely. We will hold on to our newly found Timmy shares. Wendy's portion of the business remains under-appreciated by the Street and we may add to our position if the opportunity presents itself.

Intel (NASDAQ: INTC)

Not much to say here except, FINALLY! Ok, so the market has been on a tear. But Intel seems to be on the right course again. A slew of new products are being launched and the recent layoffs and divestitures shows management can act fast and decisively. AMD (NYSE: AMD), bring it on.

Cisco (NASDAQ: CSCO)

Cisco offered a beautiful opportunity in August when it dipped below $20 after I posted my April post. The Scientific Atlanta acquisition is looking good and with broadband and content proliferating, Cisco looks to be well positioned. Recently the company uttered the D word for the first time. It's not a matter of if but rather when Cisco will pay us a dividend.

Morningstar (NASDAQ: MORN)

Not much to report here. Company recently launched a Hedge Fund section on its web site. The stock has taken a breather and briefly touched our original purchase price recently. If it goes there again, we will add to our position.

Chapparal (NASDAQ: CHAP)

The thesis remains intact here. Steel prices have cooled off a bit. But commercial construction continues apace and consolidation should play into Chaparral's hands.

Wal Mart (NYSE: WMT)

What do you know. The recent decline in gasoline prices seem to have pumped up Wal Mart shares. The company has left the German market and is in the process of figuring out how to appeal to upper scale shoppers by redesigning stores. A risky strategy which will surely cause some pain in the short-term. Still, Wal Mart's scale and competitive advantages are hard to beat. Let alone replicate.

Corning (NYSE: GLW)

As with Cisco, Corning also took a nice little dip below $20 in August. Some softness in the LCD market spooked the market. But the company is in the middle of a solid turnaround. And forget about the fiber optics business. How come nobody is talking about the clean diesel technology the company is keeping in its back pocket?

Comcast (NASDAQ: CMCSA)

The naysayers seem to be quieter these days. The company is raking in phone subscribers after a slow start. The triple play of cable, broadband and phone are panning out. So now that the capital expenditures are over and done with, the cash is rolling in. The question is what are Comcast's plans when it comes to wireless. Will another round of mega dollar investments depress the shares? The shares have had a nice run and we may take some money off the table if the opportunity presents itself.

CBS (NYSE: CBS)

Divestments continue and dividends keep on rising. Music to our ears. And the supposedly stodgy CBS broadcast the NCAA tournament online. So there.

Heinz (NYSE: HNZ)

Mr. Peltz is now sitting on the board. Not all his nominees won a seat though. Still, Heinz management is implementing many of Peltz's recommendations without any admission.

Tyco (NYSE: TYC)

The plans to break up the company appear to be on track. The recent break out of the shares is also welcome. Stay tuned on this one.

Mittal (NYSE: MT)

Mr. Mittal and Arcelor have finally made friends. The merger is going through to create the world's largest steel maker. The industry remains fragmented and global demand should remain strong. The shares did dip below $30 after my March post and have since rebounded.

Electronic Arts (NASDAQ: ERTS)

Thank you Mr. Market for the the opportunity to snap up shares in the low $40s back in Q2. Lo and behold, analysts are coming out of the wood work after the recent run-up pointing out that the industry's fortune seem to be turning around sooner than anticipated. Date point: the company's Madden NFL 2007 generated $100 million in its first week after launch!

Home Depot (NYSE: HD)

Mr. Nardelli annoyed many people with his antics during the annual shareholder meeting. The housing market's roller coaster ride and high gasoline prices havent helped much either. Still, the stock price has languished even as Nardelli has significantly boosted Home Depot's financial since he took over. Meanwhile, the company continues to pursue its strategy of catering to professional contractors through Home Depot Supply.

Posko (NYSE: PKX)

See Mittal. The thesis hasn't changed here. The shares rallied nicely after I first mentioned the company in March but have since retreated some. Posco has forged closer ties with Japan's Nippon Steel to try and thwart any takeover attempts. Meanwhile, management is shedding non-core assets and is planning to expand globally through M&A. Did I mention the company has no debt?

Walter Industries (NYSE: WLT)

I first wrote about this company back in July. Since then the stock has been on a bit of a roller coaster ride. Coal and natural gas comprise one business segment for Walter. The entire energy sector has been under pressure. On top of that Walter's coal business has not performed as well as anticipated by some of the hedge funds that had loaded up on the stock. So some of the hot money has been heading for the exits. But the thesis remains intact. The Mueller spin-off is on track and on a sum of the parts basis, the shares seem significantly undervalued at these levels.

Budweiser (NYSE: BUD)

Things are looking up for the king of beer. Volume growth seems to be picking up, labeit modestly and prices are stabilizing. Meanwhile, August Busch IV has taken the helm putting the company under family control once more. Let's hope he is ready for the challenge.

Google (NASDAQ: GOOG)

Google has been busy taking market share and cranking out more products and alliances. The shares appear range-bound for now. We need a nice hiccup to add to our position.

Centex (NYSE: CTX) and Pulte (NYSE: PHM)

It's been a wild ride. The Fed is done. The Fed is not done. Inflation is under control. Inflation will force the Fed to raise rates again. Hard landing. Soft landing. Who knows. The shares were recently trading close to book value and have rebounded some as some data seems to be suggesting that the economy is cooling enough to entice the Fed to hold tight and maybe even cut rates. Not to mention the fact that oil prices have been falling easing inflationary pressures further. Meanwhile, homebuilder after homebuilder is ratcheting down earnings estimates and singing the blues. But nobody seems to be taking the CEOs seriously when they say they are being prudent with land purchases and new building projects. Nobody seems to believe that these companies are in better finacial shape than the last housing debacle and that the big boys could be in great position to consolidate and gobble up the smaller players. To be sure, risks remain. Adjustable-rate mortgages could come back to haunt those who didn't do their homework causing many to sell at any price, causing a housing inventory glut. And maybe the Fed will have to raise rates causing consumers to delay home purchases. None of these scenarios would be good for homebuilders. But no matter. If Mr. Market offers us the shares below book value, we will gladly take them off his hands.

Berkshire Hathaway (NYSE: BRKA)

Most noteworthy recent news was Mr. Buffett's decision to give his wealth away to various charitable foundations. The main portion went to the Bill and Melinda Gates foundation. He recently visited Israel to meet the founder of Iscar for the first time. Earlier this year he bought 80% of Iscar for $4 billion. While there, he also teased investors by pointing out that Berkshire would likely acquire another 1 to 3 utilities over the next decade. Of interest was a comment about private-equity firms providing Berkshire with some competition for potential investments. No worries. Berkshire has the luxury to wait things out and be approached by the kinds of businesses it covets. Oh, one more thing, Mr. Buffett got married at the end of August to his 29 year companion Astrid Menks.

Sears Holdings (NASDAQ: SHLD)

Eddie Lampert is on the hunt. In the most recent quarterly earnings report, Mr. Lampert couldn't have been any more specific:

"Our strong financial position and cash flow generation provide us with the flexibility to capitalize on a wide range of market opportunities as they arise. In addition to investing in our business and acquiring our shares, we are prepared to invest substantial amounts of capital if we identify other attractive investment opportunities which have the potential for returns we believe appropriately compensate the Company for the associated risks." said Edward S. Lampert, Chairman of Holdings.

Stay tuned.

Wendy's (NYSE: WEN)

The spin-off is complete. On Friday Tim Hortons (NYSE: THI) was officially orphaned and will begin trading as a stand-alone beginning Monday. One more surprise, Timmy's will e added to the S&P/TSX index. This was somewhat unexpected and caught many shorts by surprise. Our bet to invest in the Wendy's shares before the eventual spin-off has paid off handsomely. We will hold on to our newly found Timmy shares. Wendy's portion of the business remains under-appreciated by the Street and we may add to our position if the opportunity presents itself.

Intel (NASDAQ: INTC)

Not much to say here except, FINALLY! Ok, so the market has been on a tear. But Intel seems to be on the right course again. A slew of new products are being launched and the recent layoffs and divestitures shows management can act fast and decisively. AMD (NYSE: AMD), bring it on.

Cisco (NASDAQ: CSCO)

Morningstar (NASDAQ: MORN)

Not much to report here. Company recently launched a Hedge Fund section on its web site. The stock has taken a breather and briefly touched our original purchase price recently. If it goes there again, we will add to our position.

Chapparal (NASDAQ: CHAP)

The thesis remains intact here. Steel prices have cooled off a bit. But commercial construction continues apace and consolidation should play into Chaparral's hands.

Wal Mart (NYSE: WMT)

What do you know. The recent decline in gasoline prices seem to have pumped up Wal Mart shares. The company has left the German market and is in the process of figuring out how to appeal to upper scale shoppers by redesigning stores. A risky strategy which will surely cause some pain in the short-term. Still, Wal Mart's scale and competitive advantages are hard to beat. Let alone replicate.

Corning (NYSE: GLW)

As with Cisco, Corning also took a nice little dip below $20 in August. Some softness in the LCD market spooked the market. But the company is in the middle of a solid turnaround. And forget about the fiber optics business. How come nobody is talking about the clean diesel technology the company is keeping in its back pocket?

Comcast (NASDAQ: CMCSA)

The naysayers seem to be quieter these days. The company is raking in phone subscribers after a slow start. The triple play of cable, broadband and phone are panning out. So now that the capital expenditures are over and done with, the cash is rolling in. The question is what are Comcast's plans when it comes to wireless. Will another round of mega dollar investments depress the shares? The shares have had a nice run and we may take some money off the table if the opportunity presents itself.

CBS (NYSE: CBS)

Divestments continue and dividends keep on rising. Music to our ears. And the supposedly stodgy CBS broadcast the NCAA tournament online. So there.

Heinz (NYSE: HNZ)

Mr. Peltz is now sitting on the board. Not all his nominees won a seat though. Still, Heinz management is implementing many of Peltz's recommendations without any admission.

Tyco (NYSE: TYC)

The plans to break up the company appear to be on track. The recent break out of the shares is also welcome. Stay tuned on this one.

Mittal (NYSE: MT)

Mr. Mittal and Arcelor have finally made friends. The merger is going through to create the world's largest steel maker. The industry remains fragmented and global demand should remain strong. The shares did dip below $30 after my March post and have since rebounded.

Electronic Arts (NASDAQ: ERTS)

Thank you Mr. Market for the the opportunity to snap up shares in the low $40s back in Q2. Lo and behold, analysts are coming out of the wood work after the recent run-up pointing out that the industry's fortune seem to be turning around sooner than anticipated. Date point: the company's Madden NFL 2007 generated $100 million in its first week after launch!

Home Depot (NYSE: HD)

Mr. Nardelli annoyed many people with his antics during the annual shareholder meeting. The housing market's roller coaster ride and high gasoline prices havent helped much either. Still, the stock price has languished even as Nardelli has significantly boosted Home Depot's financial since he took over. Meanwhile, the company continues to pursue its strategy of catering to professional contractors through Home Depot Supply.

Posko (NYSE: PKX)

See Mittal. The thesis hasn't changed here. The shares rallied nicely after I first mentioned the company in March but have since retreated some. Posco has forged closer ties with Japan's Nippon Steel to try and thwart any takeover attempts. Meanwhile, management is shedding non-core assets and is planning to expand globally through M&A. Did I mention the company has no debt?

Walter Industries (NYSE: WLT)

I first wrote about this company back in July. Since then the stock has been on a bit of a roller coaster ride. Coal and natural gas comprise one business segment for Walter. The entire energy sector has been under pressure. On top of that Walter's coal business has not performed as well as anticipated by some of the hedge funds that had loaded up on the stock. So some of the hot money has been heading for the exits. But the thesis remains intact. The Mueller spin-off is on track and on a sum of the parts basis, the shares seem significantly undervalued at these levels.

Budweiser (NYSE: BUD)

Things are looking up for the king of beer. Volume growth seems to be picking up, labeit modestly and prices are stabilizing. Meanwhile, August Busch IV has taken the helm putting the company under family control once more. Let's hope he is ready for the challenge.

Google (NASDAQ: GOOG)

Google has been busy taking market share and cranking out more products and alliances. The shares appear range-bound for now. We need a nice hiccup to add to our position.

Centex (NYSE: CTX) and Pulte (NYSE: PHM)

It's been a wild ride. The Fed is done. The Fed is not done. Inflation is under control. Inflation will force the Fed to raise rates again. Hard landing. Soft landing. Who knows. The shares were recently trading close to book value and have rebounded some as some data seems to be suggesting that the economy is cooling enough to entice the Fed to hold tight and maybe even cut rates. Not to mention the fact that oil prices have been falling easing inflationary pressures further. Meanwhile, homebuilder after homebuilder is ratcheting down earnings estimates and singing the blues. But nobody seems to be taking the CEOs seriously when they say they are being prudent with land purchases and new building projects. Nobody seems to believe that these companies are in better finacial shape than the last housing debacle and that the big boys could be in great position to consolidate and gobble up the smaller players. To be sure, risks remain. Adjustable-rate mortgages could come back to haunt those who didn't do their homework causing many to sell at any price, causing a housing inventory glut. And maybe the Fed will have to raise rates causing consumers to delay home purchases. None of these scenarios would be good for homebuilders. But no matter. If Mr. Market offers us the shares below book value, we will gladly take them off his hands.

Friday, April 21, 2006

Homes and Chips

Hi everyone.

A few ideas for you to consider. There is more on these on my own blog so I won't duplicate all the content.

Intel (Nasdaq: INTC)

Price: $19.06

I know AMD is eating their breakfast and lunch and dinner. But Intel is getting cheap. On a forward P/E basis, it is trading at the same multiple as the S&P 500. The pain for the stock may not be over, but I think it is worth taking a position at these levels. Perhaps you will get a chance to add to your position at $17 or $18. I won't bore you with the details, but you can read more about my thoughts on this on my blog.

Pulte (NYSE: PHM) and Centex (NYSE: CTX)

Price: $40 and $62)

You probably think I am crazy. But that's OK. As a value investor, I will have to get used to that. What am I thinking? With a looming armageddon in the frothy housing market, why would I recommend shares of a couple of homebuilders? Well, the simple answer is that they are CHEAP, CHEAP, CHEAP. But, surely, there is a reason they are so cheap. After all, the housing bubble will soon burst. Right? Well, I am not so sure. These companies have been around for decades and have been through many ups and downs. They are solid businesses with solid balance sheets and sound management. And did I mention they are CHEAP? Mr. Sheasby may be thinking the markets are efficient and so the shares of these companies are deservedly beaten down. Maybe. But I will side with David Dreman on this one. You can read more about Dreman on my blog so I won't bore you with the contrarian blurb. In short, homebuilders are the cheapest, by P/E, of all the major industry sectors on the market. They deserve a serious look for the long-term investor.

A few ideas for you to consider. There is more on these on my own blog so I won't duplicate all the content.

Intel (Nasdaq: INTC)

Price: $19.06

I know AMD is eating their breakfast and lunch and dinner. But Intel is getting cheap. On a forward P/E basis, it is trading at the same multiple as the S&P 500. The pain for the stock may not be over, but I think it is worth taking a position at these levels. Perhaps you will get a chance to add to your position at $17 or $18. I won't bore you with the details, but you can read more about my thoughts on this on my blog.

Pulte (NYSE: PHM) and Centex (NYSE: CTX)

Price: $40 and $62)

You probably think I am crazy. But that's OK. As a value investor, I will have to get used to that. What am I thinking? With a looming armageddon in the frothy housing market, why would I recommend shares of a couple of homebuilders? Well, the simple answer is that they are CHEAP, CHEAP, CHEAP. But, surely, there is a reason they are so cheap. After all, the housing bubble will soon burst. Right? Well, I am not so sure. These companies have been around for decades and have been through many ups and downs. They are solid businesses with solid balance sheets and sound management. And did I mention they are CHEAP? Mr. Sheasby may be thinking the markets are efficient and so the shares of these companies are deservedly beaten down. Maybe. But I will side with David Dreman on this one. You can read more about Dreman on my blog so I won't bore you with the contrarian blurb. In short, homebuilders are the cheapest, by P/E, of all the major industry sectors on the market. They deserve a serious look for the long-term investor.

Thursday, April 06, 2006

Hotels, Theme Parks, Casinos and Telecom

Ok Mr. Sparling, that is an excellent point. All those people still have to take a vacation. I presume tourism has declined due to weakness in the US dollar. Although ignoring the strength of our Canadian dollar, the USD actually held up quite well last year and appreciated against the yen and the euro.

In any case, I don't know much about casinos and the hospitality business. I do like your Disney (Nasdaq: DIS) pick though. I am not sure about their theme park business (although Disney has amazing brands - who doesn't recognize Mickey!), but Disney's recent acquisition of Pixar and the arrival of Mr. Jobs changes many things. Not to mention that gem of an asset, ESPN. I used to own Disney many years ago but let go of it because I got tired of Eisner. I don't think the shares are cheap but they are no too expensive either. There should be upside from these levels.

Incidentally, a company in the Entertainment business that I think you should consider taking a look at is CBS (NYSE: CBS). Viacom and CBS recently split up to try and unlock some value for shareholders. But the shares have declined since the IPO. CBS' businesses may be boring (radio?!), but this company is a cash machine. My brother and I have both taken a position at the mid $24 range recently.

Now to telecom. The Alcatel/Lucent "merger" makes a lot of sense for Alcatel and it gives the company access to the lucrative US market. The telecom landscape is changing at a maddening pace. Consolidation may continue. Juniper (Nasdaq: JNPR) for example may find itself in limbo unless it makes a move. Other shares have been on fire. Remember JDS Uniphase (Nasdaq: JDSU)? It has participated in the rally also. Who knows, perhaps my brother and I will finally break even after stubbornly averaging down on our position over the years. The company's management team has quietly transformed and repositioned this company.

How to play all this? I am not sure. But I can tell you what companies I like in this space. Cisco (Nasdaq: CSCO) was a screaming buy below $20 and if it goes there again, I would add to my position. I also really like Corning (NYSE: GLW). Yes the same company that got crushed because it over invested in fiber optics during the bubble. I bought Corning more than a year ago when it became apparent that the company will play a significant role in the growth of the LCD market. Corning is the largest producers of LCD glass. Its fiber optics business is still hurting, I believe, but the rest is firing on all cylinders. The management team has done a good job paying down debt and going back to its roots of innovation. For example, the compay's diesel emissions control technology is not something people think of when you mention Corning. But this technology should contribute to growth substantially in the medium term. The shares are not cheap any longer and trade at a premium to the S&P on a forward P/E basis, but you should watch for any corrections to take a position.

Finally, I like Comcast (Nasdaq: CMCSA). My brother and I have built a position in Comcast over the past year and continue to hold. Cable shares have been under pressure recently as competition from telecom and satellite heats up. The landscape is changing everyday and the companies are encroaching on each others' turfs. Telecom is providing TV while cable is providing telephone service and so on. They all have been investing billions to build up the infrastructure to be able to deliver the "quadruple play" to the cunsumer: TV, wireless, broadband and telephone. Comcast is the largest cable operator and owns my beloved Golf Channel as well as OLN. Not too long ago they made a failed bid for Disney. Clearly part of their strategy is to build the content side of the business so that they can better leverage the pipes they own into people's homes. Meanwhile, the company is generating gobs of cash and buyig back shares. And hopefully they will soon be able to reduce Capex so that Mr. Market will begin to recognize the value in this company. One more thing, at these levels, you are buying the shares at or below the levels Mr. Buffett took his position at in 2004.

So in summary, Disney looks OK to me. You should consider CBS and Comcast also, while keeping an eye on Cisco and Corning.

Ali.

In any case, I don't know much about casinos and the hospitality business. I do like your Disney (Nasdaq: DIS) pick though. I am not sure about their theme park business (although Disney has amazing brands - who doesn't recognize Mickey!), but Disney's recent acquisition of Pixar and the arrival of Mr. Jobs changes many things. Not to mention that gem of an asset, ESPN. I used to own Disney many years ago but let go of it because I got tired of Eisner. I don't think the shares are cheap but they are no too expensive either. There should be upside from these levels.

Incidentally, a company in the Entertainment business that I think you should consider taking a look at is CBS (NYSE: CBS). Viacom and CBS recently split up to try and unlock some value for shareholders. But the shares have declined since the IPO. CBS' businesses may be boring (radio?!), but this company is a cash machine. My brother and I have both taken a position at the mid $24 range recently.

Now to telecom. The Alcatel/Lucent "merger" makes a lot of sense for Alcatel and it gives the company access to the lucrative US market. The telecom landscape is changing at a maddening pace. Consolidation may continue. Juniper (Nasdaq: JNPR) for example may find itself in limbo unless it makes a move. Other shares have been on fire. Remember JDS Uniphase (Nasdaq: JDSU)? It has participated in the rally also. Who knows, perhaps my brother and I will finally break even after stubbornly averaging down on our position over the years. The company's management team has quietly transformed and repositioned this company.

How to play all this? I am not sure. But I can tell you what companies I like in this space. Cisco (Nasdaq: CSCO) was a screaming buy below $20 and if it goes there again, I would add to my position. I also really like Corning (NYSE: GLW). Yes the same company that got crushed because it over invested in fiber optics during the bubble. I bought Corning more than a year ago when it became apparent that the company will play a significant role in the growth of the LCD market. Corning is the largest producers of LCD glass. Its fiber optics business is still hurting, I believe, but the rest is firing on all cylinders. The management team has done a good job paying down debt and going back to its roots of innovation. For example, the compay's diesel emissions control technology is not something people think of when you mention Corning. But this technology should contribute to growth substantially in the medium term. The shares are not cheap any longer and trade at a premium to the S&P on a forward P/E basis, but you should watch for any corrections to take a position.

Finally, I like Comcast (Nasdaq: CMCSA). My brother and I have built a position in Comcast over the past year and continue to hold. Cable shares have been under pressure recently as competition from telecom and satellite heats up. The landscape is changing everyday and the companies are encroaching on each others' turfs. Telecom is providing TV while cable is providing telephone service and so on. They all have been investing billions to build up the infrastructure to be able to deliver the "quadruple play" to the cunsumer: TV, wireless, broadband and telephone. Comcast is the largest cable operator and owns my beloved Golf Channel as well as OLN. Not too long ago they made a failed bid for Disney. Clearly part of their strategy is to build the content side of the business so that they can better leverage the pipes they own into people's homes. Meanwhile, the company is generating gobs of cash and buyig back shares. And hopefully they will soon be able to reduce Capex so that Mr. Market will begin to recognize the value in this company. One more thing, at these levels, you are buying the shares at or below the levels Mr. Buffett took his position at in 2004.

So in summary, Disney looks OK to me. You should consider CBS and Comcast also, while keeping an eye on Cisco and Corning.

Ali.

Tuesday, March 07, 2006

An Update from AA

Hope you are all well. I thought I would do a quick update on my picks. Since I am not a big trader, I won't in general post a lot of picks. But here is an update on the stocks I have recommended in the past plus a few you should put on the radar screen or even consider taking a position in.

1. SHLD ($120.88) and PIR ($10.12)

Sears hasn't done much since I receommended it last November. But Lampert has continued with his program and seems to be making progress. I continue to like the opportunity to invest alongside Lampert especially when he has a significant amount of his net worth tied up in the company through his hedge fund.

As for PIR, it has been a wild ride. It is down about 20% since I recommended it. The stock bottomed at $8.50 recently but has bounced back nicely. I continue to like this company as a deep value play.

2. TYC ($26)

Tyco took a bit of a beating after their earnings came in below estimates and costs of restructuring were estimated by management to be on the order of $1 billion. Oh yes, and it will take the management a year to complete the split of the company into three separately traded companies about a year. All this spooked the market. One year? $1 billion?

Well, this baffles me. What did people think? They can get this done with a $5 million budget and in 6 months?! Tyco's three businesses may not be exciting (Fire and Security, Healthcare products and Electronics components). But the sum of the parts is worth more than $30. And with all the action in private equity these days, the spin-offs will be prime targets for acquirers. I continue to like the stock and my brother and I have added to our position at these levels.

3. MORN ($41)

Up about 17% since I posted and hit a high of $43 recently. The earnings came in and they were good! This company is executing well and is still under the radar. I think they will continue to grow. If the shares drop below $37, they would be worth a look to add to your position.

4. CHAP ($47)

Up about 56% since I posted and hit a high of $49 very recently. I didn't expect to see these levels for another two years. But thanks to Mr. Mittal's bid for Arcelor, steel stocks have been on fire. I still like CHAP for the long haul especially since the non-residential construction boom is still getting going. But I might take some money off the table here.

5. CWB.TO and IIC-LV.TO

CWB is up about 7% since December's recommendation. They report earnings in a few days. I still like them as a potential take-over candidate and because of a conservative management team. My brother and I are contemplating switching our position into NA.TO which has underperformed peer banks recently.

The call on ING Canada turned out well. The stock is up about 20% and they reported strong results in Feb. I continue to hold. Lots of growth opportunity ahead.

6. Energy and Materials

I continue to like the oil sands story and so PCA.TO remains a holding. As for ECA.TO, the stock has come back down to earth as natural gas prices have declined substantially. But Encana remains the largest natural gas producer in North America with exposure to the Oils Sands. If there is a severe correction, I would look to add to add to this position. My brother and I also took a small position in Goldcorp during Q4 of last year. I never posted this so I won't dwell on it here. But Gold has done spectacularly and Goldcorp has done a nice job increasing reserves and remains a low cost producer. I like the macro fundamentals behind gold and I think it will continue to do well.

On The Radar/Consider Adding

Value - Wendy's (NYSE: WEN)

Price: $60

I am not going to get into a long expose on Wendy's here. So I refer you to my own blog at http://alagheband.blogspot.com/ . We have taken a position in WEN at around $57. I personally don't see much downside in owning the shares before Tim Horton's IPO. And if my assessment is correct, you will end up owning Wendy's shares at a bargain price with room for much more appreciation post spin-off of Tim Horton's (if you are patient). I would still take a position at these levels.

Value - Heinz (NYSE: HNZ)

Price: $38

The same billionaire investor (Mr. Peltz) who nudged Wendy's management into action, is now on Heinz's case. Yes we are talking Ketchup here. Peltz is planning to nomimate 5 to the board and the stock has moved from $34 to $38 recently. Still, it has not gone anywhere in two years. It is unclear what stake Peltz's group has taken in the company, but probably he is building a position. A Barron's article this weekend noted the company could be worth $49 on a sum of the part basis. Plus, the stock pays a nice 3% dividend and can be a nice hedge against USD since 50% of revenues come from overseas. The CEO has been divesting non-core assets and buying back shares. But there may be more to squeeze out of this one. Peltz has a solid track record. I would be willing to put my money on him and initiating a position at these levels.

Value - Electronic Arts (Nasdaq: ERTS)

Price: $51

EA is the gorilla of video games. With game machines getting ever more powerful and online gaming catching on, they are in a sweet spot. Kids spend more time playing games than watching TV these days. EA and other game companies are going through a rough patch right now. Basically what is happening is that people are postponing purchases until they can get their hands on new XBox 360 and Playstation 3 consoles. Microsoft is still trying to catch up with demand and Sony's machine has been delayed into early next year (rumors). EA stock has been holding steady through all this at these levels which should mean the bad news is priced in. They have already brought down expectations during their last earnings call. My brother and I plan to take an initial position at these levels.

Value - Mittal Steel (NYSE: MT)

Price: $34

I know, yet another steel play. And frankly, I feel like we may be a bit late to this one. MT has made a nice run since the company made a bid for Arcelor. The opportunity to get in was when the stock was trading below $30. Mittal and his son have been on a tear and have quickly but quietly built Mittal into a global powerhouse. Consolidation will further insulate the company from the boom and bust cycle of the steel industry. Plus, they have managed to build a vertically integrated company with its own iron ore and coal resources. All this gives the company a competitive advantage.

The Arcelor bid is turning out to be a major battle and it's unclear how it will all turn out. Also, the Mittal's own a majority of the company. That may make you nervous. But I personally like family owned businesses. I would have loved to have initiated a position in MT below $30.

Value - Home Depot (NYSE: HD)

Price: $41.5

Yes, another boring company that sells rakes and drills. And the first words out of people's mouths are, "but the housing bubble is going to burst!". That's all fine and well. But HD is becoming more than a retailer. The CEO is expanding the company's business into services and catering to professional contractors. There are also rumors the company is sniffing for opportunities in China.

The stock has been stuck in this range even as HD's competitor Lowe's has seen its stock soaring. The plan to add new businesses is risky but I think HD can pull it off. I think this stock is a nice long-term hold if you can get your hands on it below $40.

Value - Posco (NYSE: PKX)

Price: $60

Goodness, another steel play. Seriously, this is just coincidence. My brother had come up with the idea of buying a Korean index fund. After a bit of research we determined that we owned some Korean shares through a emerging markets index fund we already owned. So we did some digging and came up with Posco. They are THE steel company in Korea and have a monopoly on the market. As may be expected, the shares are cheap relative to other global steel players. This is the "Korea Discount". Moreover, PKX has underperformed the Korean stock market by a wide margin over the past year.

As you may have noticed Carl Icahn has recently forayed into Korea and trying to buy out the country's largest tobacco company because he thinks the stock is undervalued. Other 'experts' have also noted that the Korean market is undervalued relative to Japan and Hong Kong. Just today, the Wall Street Journal Asia had an article saying Posco could become the target of the next activist looking to prop up the shares. The company owns many ancillary businesses which can be divested. It has no debt and a nice pile of cash also. And its dividend could be increased significantly.

This would have been a nice pick up in the mid $50 range before they started moving amidst word of Mittal's bid for Arcelor. But my brother and I might take an initial position at these levels.

That's all for now.

Ali.

1. SHLD ($120.88) and PIR ($10.12)

Sears hasn't done much since I receommended it last November. But Lampert has continued with his program and seems to be making progress. I continue to like the opportunity to invest alongside Lampert especially when he has a significant amount of his net worth tied up in the company through his hedge fund.

As for PIR, it has been a wild ride. It is down about 20% since I recommended it. The stock bottomed at $8.50 recently but has bounced back nicely. I continue to like this company as a deep value play.

2. TYC ($26)

Tyco took a bit of a beating after their earnings came in below estimates and costs of restructuring were estimated by management to be on the order of $1 billion. Oh yes, and it will take the management a year to complete the split of the company into three separately traded companies about a year. All this spooked the market. One year? $1 billion?

Well, this baffles me. What did people think? They can get this done with a $5 million budget and in 6 months?! Tyco's three businesses may not be exciting (Fire and Security, Healthcare products and Electronics components). But the sum of the parts is worth more than $30. And with all the action in private equity these days, the spin-offs will be prime targets for acquirers. I continue to like the stock and my brother and I have added to our position at these levels.

3. MORN ($41)

Up about 17% since I posted and hit a high of $43 recently. The earnings came in and they were good! This company is executing well and is still under the radar. I think they will continue to grow. If the shares drop below $37, they would be worth a look to add to your position.

4. CHAP ($47)

Up about 56% since I posted and hit a high of $49 very recently. I didn't expect to see these levels for another two years. But thanks to Mr. Mittal's bid for Arcelor, steel stocks have been on fire. I still like CHAP for the long haul especially since the non-residential construction boom is still getting going. But I might take some money off the table here.

5. CWB.TO and IIC-LV.TO

CWB is up about 7% since December's recommendation. They report earnings in a few days. I still like them as a potential take-over candidate and because of a conservative management team. My brother and I are contemplating switching our position into NA.TO which has underperformed peer banks recently.

The call on ING Canada turned out well. The stock is up about 20% and they reported strong results in Feb. I continue to hold. Lots of growth opportunity ahead.

6. Energy and Materials

I continue to like the oil sands story and so PCA.TO remains a holding. As for ECA.TO, the stock has come back down to earth as natural gas prices have declined substantially. But Encana remains the largest natural gas producer in North America with exposure to the Oils Sands. If there is a severe correction, I would look to add to add to this position. My brother and I also took a small position in Goldcorp during Q4 of last year. I never posted this so I won't dwell on it here. But Gold has done spectacularly and Goldcorp has done a nice job increasing reserves and remains a low cost producer. I like the macro fundamentals behind gold and I think it will continue to do well.

On The Radar/Consider Adding

Value - Wendy's (NYSE: WEN)

Price: $60

I am not going to get into a long expose on Wendy's here. So I refer you to my own blog at http://alagheband.blogspot.com/ . We have taken a position in WEN at around $57. I personally don't see much downside in owning the shares before Tim Horton's IPO. And if my assessment is correct, you will end up owning Wendy's shares at a bargain price with room for much more appreciation post spin-off of Tim Horton's (if you are patient). I would still take a position at these levels.

Value - Heinz (NYSE: HNZ)

Price: $38

The same billionaire investor (Mr. Peltz) who nudged Wendy's management into action, is now on Heinz's case. Yes we are talking Ketchup here. Peltz is planning to nomimate 5 to the board and the stock has moved from $34 to $38 recently. Still, it has not gone anywhere in two years. It is unclear what stake Peltz's group has taken in the company, but probably he is building a position. A Barron's article this weekend noted the company could be worth $49 on a sum of the part basis. Plus, the stock pays a nice 3% dividend and can be a nice hedge against USD since 50% of revenues come from overseas. The CEO has been divesting non-core assets and buying back shares. But there may be more to squeeze out of this one. Peltz has a solid track record. I would be willing to put my money on him and initiating a position at these levels.

Value - Electronic Arts (Nasdaq: ERTS)

Price: $51

EA is the gorilla of video games. With game machines getting ever more powerful and online gaming catching on, they are in a sweet spot. Kids spend more time playing games than watching TV these days. EA and other game companies are going through a rough patch right now. Basically what is happening is that people are postponing purchases until they can get their hands on new XBox 360 and Playstation 3 consoles. Microsoft is still trying to catch up with demand and Sony's machine has been delayed into early next year (rumors). EA stock has been holding steady through all this at these levels which should mean the bad news is priced in. They have already brought down expectations during their last earnings call. My brother and I plan to take an initial position at these levels.

Value - Mittal Steel (NYSE: MT)

Price: $34

I know, yet another steel play. And frankly, I feel like we may be a bit late to this one. MT has made a nice run since the company made a bid for Arcelor. The opportunity to get in was when the stock was trading below $30. Mittal and his son have been on a tear and have quickly but quietly built Mittal into a global powerhouse. Consolidation will further insulate the company from the boom and bust cycle of the steel industry. Plus, they have managed to build a vertically integrated company with its own iron ore and coal resources. All this gives the company a competitive advantage.

The Arcelor bid is turning out to be a major battle and it's unclear how it will all turn out. Also, the Mittal's own a majority of the company. That may make you nervous. But I personally like family owned businesses. I would have loved to have initiated a position in MT below $30.

Value - Home Depot (NYSE: HD)

Price: $41.5

Yes, another boring company that sells rakes and drills. And the first words out of people's mouths are, "but the housing bubble is going to burst!". That's all fine and well. But HD is becoming more than a retailer. The CEO is expanding the company's business into services and catering to professional contractors. There are also rumors the company is sniffing for opportunities in China.

The stock has been stuck in this range even as HD's competitor Lowe's has seen its stock soaring. The plan to add new businesses is risky but I think HD can pull it off. I think this stock is a nice long-term hold if you can get your hands on it below $40.

Value - Posco (NYSE: PKX)

Price: $60

Goodness, another steel play. Seriously, this is just coincidence. My brother had come up with the idea of buying a Korean index fund. After a bit of research we determined that we owned some Korean shares through a emerging markets index fund we already owned. So we did some digging and came up with Posco. They are THE steel company in Korea and have a monopoly on the market. As may be expected, the shares are cheap relative to other global steel players. This is the "Korea Discount". Moreover, PKX has underperformed the Korean stock market by a wide margin over the past year.

As you may have noticed Carl Icahn has recently forayed into Korea and trying to buy out the country's largest tobacco company because he thinks the stock is undervalued. Other 'experts' have also noted that the Korean market is undervalued relative to Japan and Hong Kong. Just today, the Wall Street Journal Asia had an article saying Posco could become the target of the next activist looking to prop up the shares. The company owns many ancillary businesses which can be divested. It has no debt and a nice pile of cash also. And its dividend could be increased significantly.

This would have been a nice pick up in the mid $50 range before they started moving amidst word of Mittal's bid for Arcelor. But my brother and I might take an initial position at these levels.

That's all for now.

Ali.

Subscribe to:

Posts (Atom)